2019 – 4th Quarter Newsletter

With the 4th quarter of 2019 upon us, it is time to start planning for the upcoming year. There is plenty of talk regarding a pending recession, tax planning and much more. Please enjoy our quarterly newsletter addressing a few of these items.

COMMERCIAL REAL ESTATE NEWS

Is a Recession Imminent? Consumers Don’t Think So

Another quarter is quickly coming to a close and headlines are predicting economic peril. But consumers aren’t worried—they’re spending more.

JP Morgan Chase – Full Article Here

Opportunity Zones: How Can They Benefit You as a Real Estate Investor?

There is a lot of talk about Opportunity Zones. Frankly, it is mostly more talk than action now, though that is changing. Real estate investors had not been provided much specific guidance from the IRS on what they can do with Opportunity Zones and how the near + long term mechanics of them work. There is enough info out there now, though still a few open questions. Some investors are jumping in to reap the benefits.

Bonvolo Real Estate Investments – Full Article Here

Mastering Multifamily Maintenance Challenges

Experts weigh in on best practices for finding, training and retaining the skilled maintenance techs that every multifamily property needs.

Chase / JP Morgan – Full Article Here

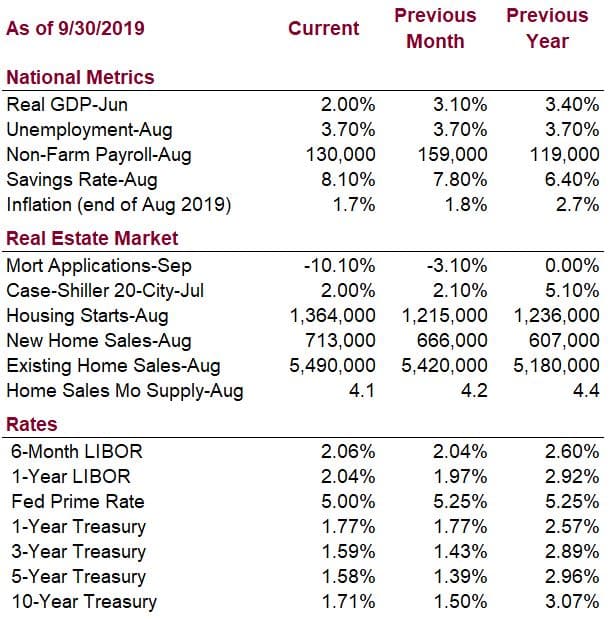

ECONOMIC DATA

BORROWER EDUCATION

30/360 vs Actual/360 vs Actual/365: Loan Accrual Calculations Explained

Believe it or not, there is more than one way to calculate the interest portion of a loan payment. Borrowers should be careful to read their loan documents to know how interest will be applied. Different methods can have a significant difference in how much interest is paid over time.

Many of us are used to simple interest, which is the method used on auto loans and credit cards. The amount of interest charged is calculated as follows:

Balance X Rate / 365 X Number of Days since last payment = Interest portion of payment.

Most commercial loans and mortgages use amortizing payments. The payment is due on the same date every month (usually the first) and interest is calculated for the period between due dates, regardless of when payment is actually made. However, there are still different methods of interest calculation that can change the interest portion of the payment.

30/360 assumes there are 360 days in a year, and each month has the same number of days. This method charges the least amount of interest over time because the daily rate (rate / 360) is applied to a 360 day borrowing period (30 X 12). The method was used before calculators were invented because it is easier to calculate: the rate can simply be divided by 12 to get a monthly rate.

Actual / 360 divides the rate by 360 to get a daily rate and multiplies by the actual number of days in a month. Over the course of a year, the daily rate is applied to 365 borrowing days. Therefore, the borrower pays more interest over the life of the loan than in either of the other methods.

Actual / 365 divides the rate by 365 to find the daily rate, then multiplies by the actual number of days in a month. This method is the most accurate of the methods. The borrower pays slightly more in interest over time under this method than under the Actual / 360 method.

At AAI Financial, we assist our client borrowers by carefully reviewing all lender documentation and helping them understand the various terms and conditions to which they are agreeing.

RECENTLY FUNDED TRANSACTIONS

Here are examples of opportunities we assisted our clients with last quarter:

- $3,494,000 2 Gas Stations, Refinance in WA – 65% LTV

- $1,730,000 Real Estate Secured Line of Credit in Southern CA – 70% LTV

- $458,200 Restaurant Real Estate and Business Acquisition in Selah, WA – SBA 7a 90% LTV

Let's talk.

We are knowledgeable, easy to talk to, and give free advice.

Please contact us to see how we can work together.

Or email us.