2021 – 2nd Quarter Newsletter

2021 is shaping up to be a year of change with new leadership in Washington, COVID-19, the opening of the economy and rising interest rates. Please enjoy our quarterly newsletter addressing these issues and more.

COMMERCIAL REAL ESTATE NEWS

Analysis: COVID-19 Relief Signals New CRE Policy Regime

“The newly enacted $1.9 trillion COVID-19 relief package should provide a short-term boost to the commercial real estate industry segments most affected by the pandemic. More broadly, however, it signals the new wave of federal policies that are in store over the next several years.”

Commercial Property Executive – Full Article Here

Lumber Prices Stalling Much Needed Multifamily and Affordable Housing Supply

“Housing demand has remained high throughout the COVID-19 pandemic, as people across the United States have rethought the concept of home and where and how they want to live. Single-family builders especially have had an increasingly hard time meeting this demand, as material prices — especially lumber — have continued to rise at unprecedented rates.”

National Association of Home Builders – Full Article Here

The Benefits of Section 1031 No One’s Talking About

“Very few people outside of the commercial real estate industry understand Section 1031 of the United States Internal Revenue Code. In turn, its long list of benefits to our economy is rarely mentioned in conversation.”

Commercial Property Executive – Full Article Here

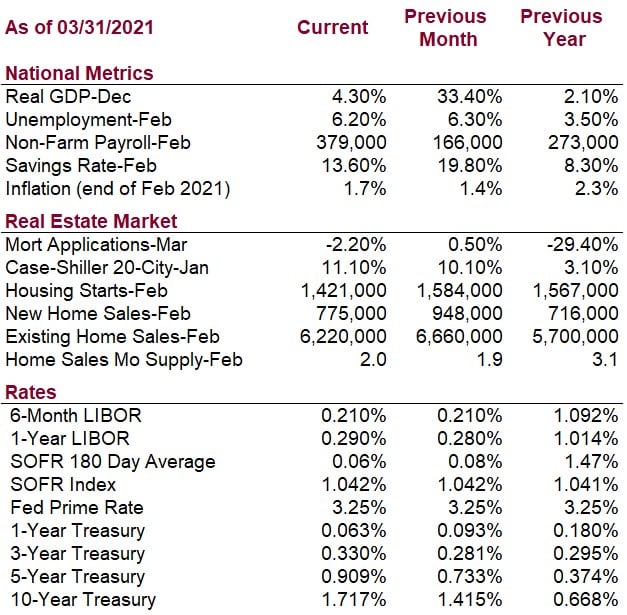

ECONOMIC DATA

In future publications of the AAI Quarterly Newsletter, LIBOR rates will no longer be published.

LIBOR is a frequent interest rate reference used in both lending and borrowing contracts. LIBOR is published daily and is calculated from hypothetical borrowing transactions submitted by a few banks. Because the transactions are hypothetical (not market-based) and may have few submissions (not an active market), LIBOR is not fully supported by an active market of observable transactions by market participants.

The LIBOR manipulation scandal of 2008 caused many to question LIBOR as a reliable interest rate benchmark. In 2017 in the United States, the Alternative Reference Rates Committee (ARRC), convened by the Federal Reserve Board, officially endorsed the Secured Overnight Financing Rate (SOFR) as the preferred benchmark interest reference rate replacing LIBOR. SOFR’s price is based on borrowing rates for overnight U.S. Treasury repurchase agreements, or repos.

On March 5, 2021, the Financial Conduct Authority, the financial services regulator in the UK, announced the cessation of LIBOR.

Articles With More Information

End of LIBOR: How to Prepare

FCA Announcement

BORROWER EDUCATION

Why Lenders Collect Tax Returns

Tax returns are collected by commercial lenders primarily to verify income. Generally, the income and expenses reported to the government for tax purposes can be relied upon to be accurate. Tax returns for small business are often prepared by a third-party CPA or accountant, which provides another level of verification that the income reported is reliable.

A lender’s primary concern when underwriting is to determine if the borrower generates sufficient cash flow to make payments on the requested loan. Business tax returns provide lenders with sufficient information to determine the cash flows of the business. Multiple years of tax returns allow the lender to see trends in the business and the direction the business is headed.

Personal tax returns can reveal important information about the guarantors. A lender will want to know, if the business is unable to make a loan payment, does the guarantor have resources to be able to step up and cover payments for a short period of time. Tax returns also allow the lender to see other sources of income or required expenses such as alimony.

Having reliable income information is important to lenders in order to accurately determine if the borrower can afford to repay the debt that has been requested.

Articles With More Information

3 Reasons Lenders Look At Tax Returns

What Lenders Review On Your Business Tax Returns

RECENTLY FUNDED TRANSACTIONS

Here are examples of opportunities we assisted our clients with last quarter:

- $3,400,000 Owner Occupied Medical Office Purchase SBA – Yakima, WA – 85% LTV

- $521,500 Gas Station / Convenience Store Purchase SBA – Yakima, WA – 90% LTV

- $2,200,000 16 Unit Multifamily Refi, FNMA Non-Recourse – Moses Lake, WA – 70% LTV

Contact us to learn how we can help you with your commercial property financing.

We’re Hiring!

AAI Financial Group continues to grow! We are looking for Loan Originators to join our team and participate in our continued success. For more information, email us at info@aaifg.com or view our career opportunities here.

Let's talk.

We are knowledgeable, easy to talk to, and give free advice.

Please contact us to see how we can work together.

Or email us.